Blog

Read my writing about Business, Insolvency, Turnaround, and the Economy.

Labour Force Update

Hot on the heels of wage price index release yesterday, we have Labour Force data out form the ABS today:

📎 Unemployment is down to 3.4%

📎 Australia created 32,200 new jobs

📎 Underemployment rate stayed at 6.0%

📎 Full time jobs were up 16,800.

This is a great jobs report and shows continued strength in the Australian jobs market (and this time we have no sample group distortions throwing out the figures).

On the back of the encouraging print for the Wage Price Index yesterday, this is really good news for workers. The continued labour market tightness should lead to further wage increases.

From an RBA perspective, this print is right on line with the RBA's forecasts and shouldn't have any impact on the RBA's interest rate decision.

September quarter wages grow more than expected

The wage prices index is out for the September quarter, with wage growth coming higher than expected:

👷🏻♀️ Wages rose 3.1% YoY and 1.0% QoQ.

👷🏻♀️ Private sector wages rose 3.4% YoY and 1.2% QoQ.

👷🏻♀️ Public sector wages rose 2.4% YoY and 0.6% QoQ.

👷🏻♀️ Wage growth including bonuses was up 3.8% YoY and 1.4% QoQ.

Four things we can learn from this print.

First, wage growth is finally starting to pick up after a long period in the doldrums. Given the tight labour market Australia has been experiencing, this is not a surprise.

Second, public sector wage deals are really stating to hold back wage growth, with public sector growth now well behind private sector growth. This is something governments can directly address.

Third, real wage growth is still sharply negative, running -3.8% YoY and -0.8% QoQ, meaning wages earners continue to go backwards in real terms.

Fourth, jobs covered by individual arrangements made up the majority of wage growth. Again, this isn't a surprise. Individual deals are often shorter term and are able to react to market changes more quickly, but it does highlight some of the deficiencies in out collective bargaining systems.

While higher wage growth is a good development for the economy, real wage growth is still sharply negative and there is little risk of wage growth significantly contributing to inflation any time soon. While this print is higher than expected, I don't see it having any impact on the RBA's current interest rate trajectory.

US October Inflation Moderates

Some better inflation news out of the USA overnight, with inflation figures for October coming in below expectation.

⭐️ Headline inflation moderated to 7.7% YoY

⭐️ Headline inflation was up only 0.4% MoM

⭐️ Core inflation is at 6.3% YoY

⭐️ Core inflation was up 0.3% MoM

While inflation is still way above where the Federal Reserve wants it to be, and we can't make judgements based on a single monthly print, it's encouraging to see the pace of inflation slowing.

In particular, core goods inflation continues to fall, while core services inflation has risen less than anticipated.

Off the back of this lower than expected print, the market is now anticipating a 50bp increase in interest rates by the Fed at their December meeting, which makes sense to me. With signs the tide may be starting to turn, slowing down a bit and waiting to see how things develop makes some sense.

Insolvency appointments remain low

However, we’re headed for recession and more insolvency appointments.

Another quarter has flown by and it’s time to take another look at how insolvency appointment numbers are tracking and look into our crystal ball to see what the future might hold.

The current picture

First, let’s look at where insolvency appointments are at the moment.

Corporate insolvency

Corporate insolvency appointments are up.

In the first quarter of FY2023 appointments were up 60% on the same period last year and were much closer to historical levels than they have been over the last two years, with appointments averaging 840 per-month over the last three months.

Of particular note is the growing popularity of small business restructuring (SBR). So far this year, we have had 83 SBR appointments, more than we had in the first eighteen months following the introduction of SBRs.

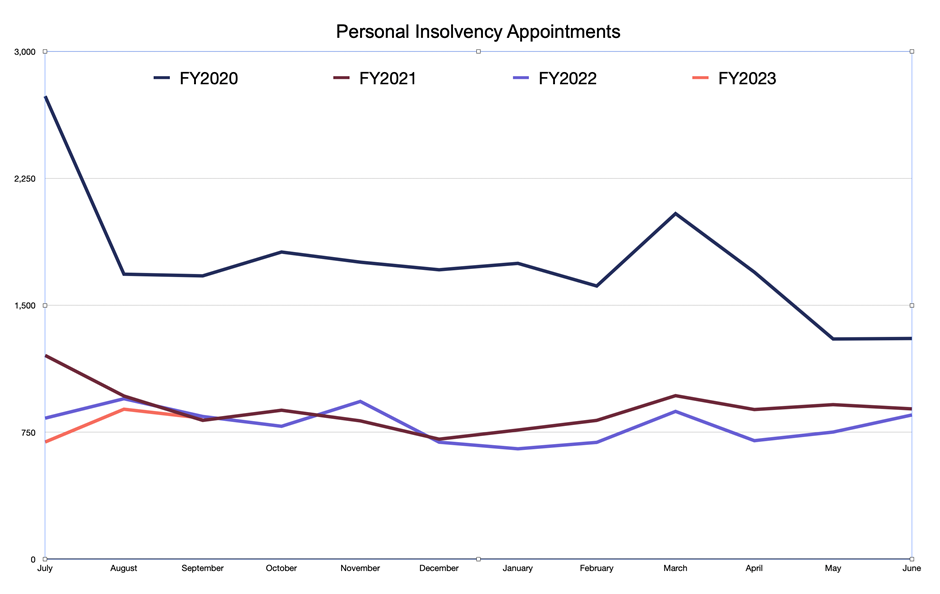

Personal insolvency

Personal insolvency appointments remain low.

In stark contrast to corporate insolvency appointments, personal insolvency appointments this financial year are lower than ever. This continues the depressed appointment numbers we have had over the last two years.

A strong economy

So, what’s going on? Why—Despite all the years of lockdowns, talk of zombie companies and business stress, and muted economic difficulties—has the number of insolvency appointments remained well below historical trends?

The main reason is, despite some headwinds, Australia’s economy is doing well and as long as this continues, insolvency appointments are likely to stay below the trend.

Business conditions remain strong

Business conditions, as measured by the NAB Quarterly Business Survey[iii] remain well above average. While businesses are facing some headwinds, in particular difficulties with staffing, the availability and cost of some supplies, and rising interest rates, trading conditions are good, which is keeping businesses from failing.

Consumer spending

Further to generally good business conditions, household spending remains very strong and well ahead of trend. Consumer spending has been elevated for all of 2022 so far, as low unemployment and strong household balance sheets have allowed people to get out and spend money at record rates.

I expect this trend to continue well into 2023. Australian households still have a huge war chest of excess savings (about $294 billion) , built up over the pandemic period, to deploy before they will be forced to tighten their belts.

Downside risks

Unfortunately, it’s not all good news. While the economy is doing well currently, businesses and households will face significant challenges over the longer run that will lead to an increase in insolvency appointments over the next two years.

ATO debt collection

The Australian Taxation Office (ATO) restarted its debt collection processes, after a long hiatus during the pandemic period. As at December 2021, the ATO's debt book was $61.4B, up 16% from the year before; and the ATO will need to work through and collect this debt over the coming years. The ATO has issued about 7,000 director penalty notices (DPNs) this year and is issuing more at a rate of 300/ business day. The ATO has also recommenced filing wind up applications. The ATO has filed 35 wind up applications so far this financial year, already a significant increase on the 10 filed in all of FY 2020-21, but still a long way short of the 3,571 the ATO filed in FY2015-16.

This pressure will have a dual impact on insolvency appointments. First, direct pressure, as the ATO pushes businesses into an insolvency appointment following its debt collection activities; and secondly, as other creditors who have also withheld from firmer debt collections activities, now feel comfortable resuming firmer action following the ATO’s.

Inflation and interest rates

Inflation continues to be a problem, with the most recent result, for September, showing inflation running at 7.3% per annum and continuing to accelerate. Forecasts are for inflation to remain well above the RBA’s target range of 2.00% to 3.00% for two more years.

As a result, we will see interest rates continue to rise as the RBA takes action to bring inflation back down to the target range. Currently, the RBA’s cash rate is 2.60%. However, markets are implying we will see a peak rate for 4.20% in late 2023. This will place significant pressure on household budgets, which will flow through to business conditions.

Real wages are falling fast

The other downside risk for household spending, and thus the fundamentals underpinning the entire economy, is the rapid fall we are seeing in real wages. A combination of sluggish wage growth and high inflation has seen real wages fall to 2010 levels over the last 18 months.

This fall in real wages (especially if it continues) will eventually flow through to household spending and lead to a significant decline in business conditions, leading to more corporate and personal insolvency.

Recession?

The final factor that will lead to increased insolvency appointment numbers over the next two years is that our economy is very likely to slip into recession near the end of 2023 or in early 2024. The historical precedent is clear, periods of high excess inflation always require a recession to being broad-based inflation under control.

The global economy is slowing and likely going into recession in mid-2023 combined with domestic factors driven by a combination of households exhausting excess savings, declining real wages, and rising unemployment and interest rates will continue to put pressure on household budgets; leading to a decline in consumer spending and conditions for business, which will ultimately push our economy into a short recession.

While a recession will lead to higher insolvency appointment numbers, I do not expect to see levels as high as we saw during previous downturns.

It’s pretty clear that a downturn is coming, and the current positive trading conditions will allow many businesses to take steps to position themselves to better weather the storm, and I also expect the recession to be relatively short and shallow, meaning the impact will be limited.

References

[i] Australian Securities and investments Commission – insolvency Statistics (current) – Series 2 - https://asic.gov.au/regulatory-resources/find-a-document/statistics/insolvency-statistics/insolvency-statistics-current/

[ii] Australian Financial Security Authority - monthly personal insolvencies - https://www.afsa.gov.au/about-us/statistics/monthly-personal-insolvency-statistics

[iii] NAB Quarterly Business Survey - September 2022 - https://business.nab.com.au/nab-quarterly-business-survey-september-2022-56500/

[iv] ANZ Research - https://www.anz.com/institutional/our-expertise/anz-research/

[v] ASX - https://www.asx.com.au/data/trt/ib_expectation_curve_graph.pdf

Federal Reserve increases rates 75bp

Overnight the Fed raised rates in the USA by another 75bp to a target range of 3.75% to 4.00%. This was not a surprise, a fourth consecutive 75bp rise had been widely anticipated, as inflation indicators in the USA stubbornly refuses to roll over.

While there was some new wording in the Fed's statement, which hinted that we may be approaching a slow down in the hiking cycle, Powell made it very clear in his press conference, that it was far to early to be talking about a pause in the rate cycle.

“What I am trying to do is make sure our message is clear, which is that we think we have a ways to go, we have some ground to cover with interest rates, before we get to that level of interest rates that we think is sufficiently restrictive,” Powell said.

What this means is the Fed may slow the pace of rate increases going forward, but expects the terminal rate to be higher, and to be with us for longer, than previous forecasts.

For Australia this likely means more pressure on the Australian dollar as the Fed continues to raise rates faster than the RBA.

High resource prices, coupled with strong resource demand, have kept the AUD from falling too far during this hiking cycle. However, there are signs that some of that resource demand is coming off, and without that support, or a more hawkish turn from the RBA, I expect the AUD to slip further.

RBA Increases rates 25bp

The RBA increased interest rates by another 25bp to 2.85% this afternoon, continuing along the cautious path they pivoted to last month, as was widely expected.

However, the bigger news was the revised inflation forecasts in the RBA's statement. The RBA now expects inflation to peak above 8% later this year, and stay above 4.75% in 2023, and won't fall below 3% at all in 2024. That is, inflation will be higher, for longer, and the RBA (bizarrely) doesn't seem to mind.

There really isn't a lot of sense to the RBA's approach. Higher inflation for longer is bad for the economy and households. The RBA could shorten this cycle by raising rates further and faster.

I'm still expect the RBA will have to raise the cash rate to around 4.20% to tame inflation and there is nothing to be gained getting there slowly and stretching out the period of excess inflation and the damage it causes to household incomes and balance sheets.

September Quarter Inflation

An absolutely terrible CPI print today, with inflation way ahead of expectations in the September quarter.

🔥 Headline inflation was 7.3% YoY (vs 7.0% expected)

🔥 Trimmed mean inflation was 6.1% YoY (vs 5.6% expected)

🔥 The preliminary monthly core inflation print was up 6.8% YoY

🔥 Inflation for the September quarter was 1.8% QoQ

🔥 Non-discretionary inflation accelerates to 8.42% which will hit household budgets hard

🔥 Inflation is now broadly entrenched across the economy, with 83% of the basket increasing at more than 2.5% YoY

This is all pretty bad news for the economy, with inflation rising faster than expected. There's reasons for concern looking forward, with services inflation currently only making up 1.7% of the 7.3% YoY increase, there is a lot of scope for services inflation to grow (as we've seen in the US) and keep inflation high for an extended period.

While this print 'should' push the RBA to increase the pace of rate rises back up to 50bp a months, I suspect it won't and we'll see another 25bp move next week.

Instead, we are likely to see a longer and slower hiking cycle with a higher terminal rate around 4.2% late next year.

Budget Thoughts

A good solid budget by the government last night with nothing large or surprising. Which was exactly what was needed. A few quick observations:

✅ Great to see some fiscal responsibility after the wild excesses of the last government. Very little in the way of extra spending and banking most of the tax windfall from inflation and resources will make the RBA’s job battling inflation easier.

✅ Extra funding for tax enforcement and compliance is long overdue and fantastic to see. Unfortunately, opportunities for more substantive tax reform were passed over in this budget.

✅ Improvements to both childcare funding and paid parental leave are excellent and should be a tiny step in the direction of reducing genders based imbalances in the workforce.

✅ Not at all surprising given the parliament enquiry that is ongoing, but no changes announced in the budget for Australia's insolvency regime.

The framing of the budget was very much setting up for tax increases and spending cuts over the rest of Labour's term. While it's never nice to contemplate paying more tax, given the budget position Australia has, more tax revenue is going to be an unwelcome necessity.

On the positive side, this budget nicely balanced new spending with cuts in other areas. I'm hopeful this presages a similar approach in future budgets rather than a return to a tax and spend mentality.

Continued signs of strong inflation

A few more data points this morning that point towards inflation staying elevated and signalling that the RBA needs to do more with rate rises to slow the economy.

First, ANZ Research shows consumers spending continues to be well above trend, with no noticeable slowdown so far in 2022. I've previously highlighted the strong savings Australian households have, which will allow them to keep spending elevated long after interest rate increases start to bite (which the haven't yet). I expect we will be well into 2023 before we see a downturn in consumer spending on the current trajectory.

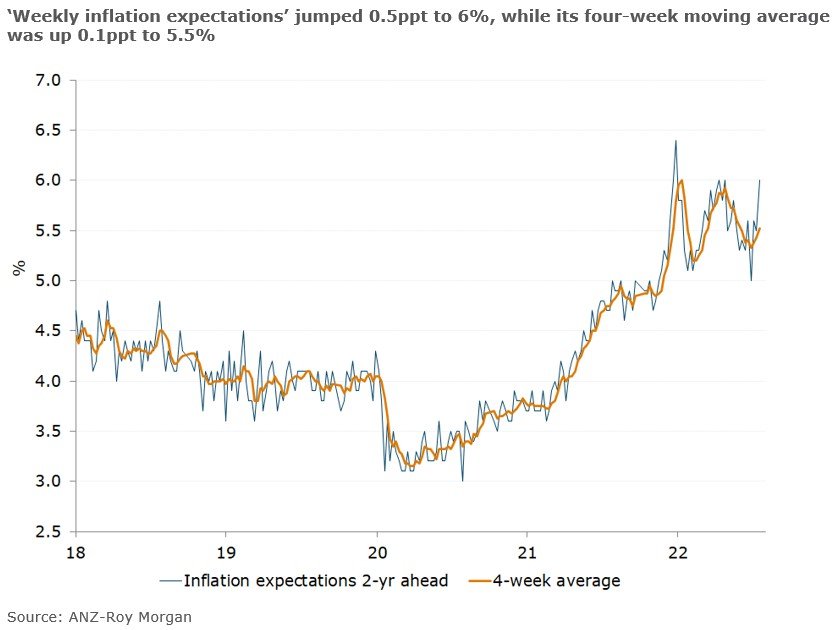

Second, inflation expectations (per ANZ-Roy Morgan) where up 0.5% to 6% in the wake of the RBA's dovish pivot. A clear demonstration of the risks associated with showing weakness and taking the foot of the gas when battling inflation. Higher inflation expectations tend to filter through as higher future inflation.

While the key data point for the RBA will be CPI figures out next week, it's looking increasingly likely that the 25bp increase this month was a mistake and an outsized 'catch-up' increase of 75bp will be the pragmatic move next month.

Putting housing price falls into perspective

Falls in real estate prices need to be put into perspective.

You can't open a news website at the moment without seeing endless hyperventilating about the 'crash' in real estate prices and you'd think, based on all the column inches dedicated to is, that falls in house prices were really important. But they have hardly any impact on most households or the real economy.

First, falls in asset prices only matter in real terms if the asset is sold and those falls in value are crystallised. As long as the asset stays in use and the 'loss' is never crystallised, the 'value' placed on the assets is irrelevant. Most real estate only gets sold VERY infrequently. The average time to hold real estate is over 12 years.

There are about 10.8 million houses in Australia. In an average year, only 500,000 of these houses actually get sold. When prices are falling the turnover rate also falls. Household aren't required to mark asset prices to market, and the incidence of forced sales by banks foreclosing in Australia is very low. So while the 'value' of a household's real estate may fall, the practical impact on most (95% or more) households in nothing.

Second, the vast majority of Australian properties are still well in the black. House prices have seen steady growth in value over the last several decades before the TFF fuelled boom in 2021. Only about 1.1 million houses have changed hands since January 2021. That means the more than 90% of properties were purchased at pre-2021 prices and we would need to see falls in value of more than 20% before any of these properties would actually be losing money if sold. More than 50% of properties have been held for more than 10 years, meaning they were bought at prices less than half of the peaks prices we saw in 2022.